-

My Partner Doesn’t Know I’m in Debt. What Should I Do?

My partner doesn’t know I’m in debt. What should I do? Being in debt without your partner knowing can feel frightening. You might be worried they’ll be angry, disappointed, or that it could change how they see you. Debt can feel even harder when you’re carrying it alone. You may be hiding letters, avoiding conversations,…

-

Skipping Meals to Pay Bills? What To Do Next

Skipping meals to pay bills: what to do if you can’t afford food and bills Skipping meals so you can pay bills is a sign that your budget is under serious pressure. It doesn’t mean you’ve failed. It means the cost of essentials may now be more than your income can cover. Recent research from…

-

How to talk to kids about money

How to talk to kids about money Talking to children about money can feel uncomfortable, especially if money feels tight in your own household. You might worry they’re too young or feel unsure what to say. You don’t need to be an expert to talk to kids about money in a helpful way. The most…

-

Why do I compare myself to others financially?

It’s hard not to compare your finances to other people’s. It can sometimes feel like everyone else is doing better with money — saving more, spending more comfortably, or moving ahead faster.

-

Managing family finances on a tight budget

Managing family finances on a tight budget Managing family finances on a tight budget can feel hard, especially when food, energy, rent, mortgage payments and childcare costs are taking up more of your income. Recent data from the Money and Pensions Service shows that 49% of UK adults are struggling to keep up, falling behind,…

-

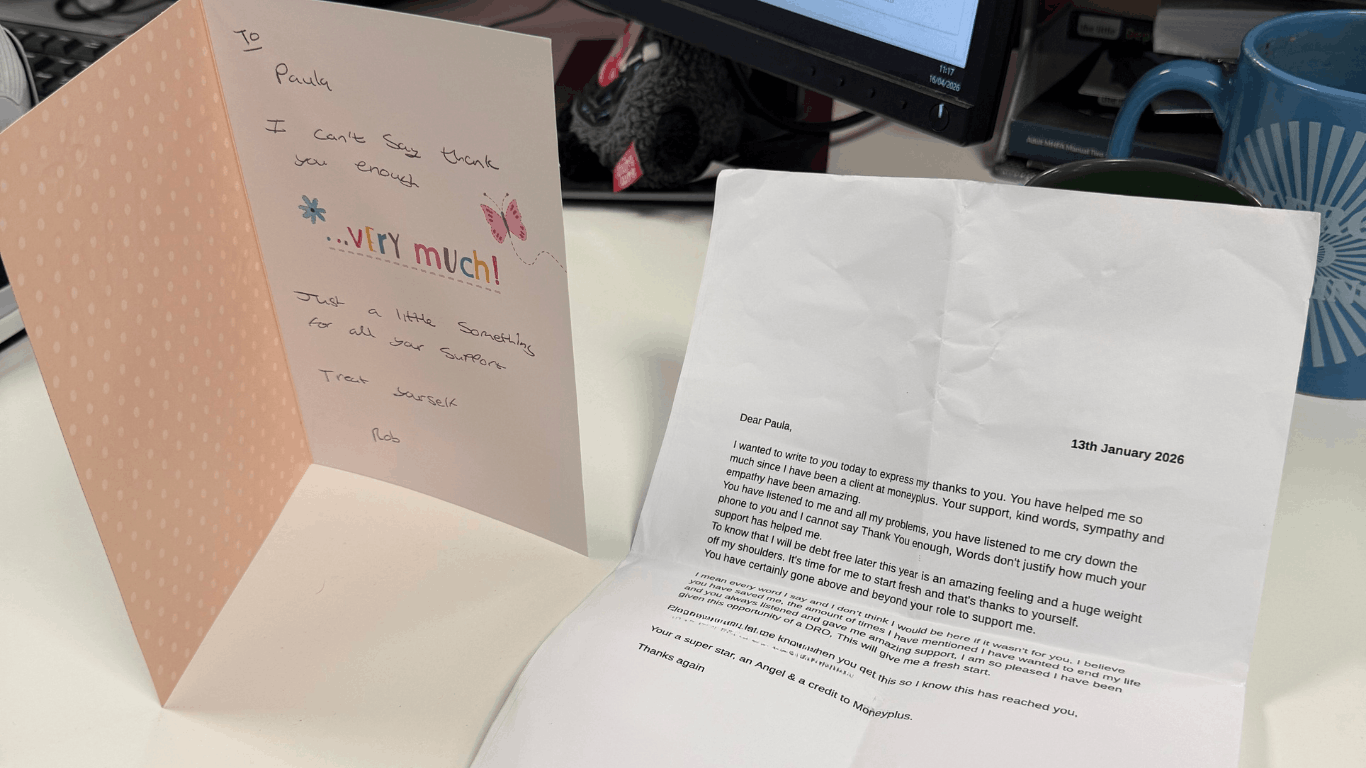

Behind the MoneyPlus People: A thank you card for Paula

Behind the MoneyPlus People: A thank you card for Paula Welcome to our new blog series – Behind the MoneyPlus People. This series will be a place for us to share the incredible work our MoneyPlus people do every day, and to celebrate how these wins are positively impacting our customers. Last week, one of…

-

Debt consolidation vs Debt Management Plan (DMP) | key differences explained

Debt consolidation vs debt management plan: what’s the difference? Debt consolidation and Debt Management Plans (DMPs) are two ways to manage multiple debts. With debt consolidation, you take out new credit, such as a loan or credit card, to pay off existing debts. Debt consolidation is more commonly used by people who can still access…

-

Student loans are changing: what this means for you

The UK government has announced that some student loans in England and Wales will have their interest rates capped at 6% beginning from September 2026. At first glance, this may sound like positive news. But what does it actually mean for you and your money? Let’s break it down in a simple, clear way. Interest on your Plan 2 student loans and postgraduate loans will be capped From September 2026, interest on Plan 2 student loans and postgraduate…

-

UK household debt levels hit £67,350 in 2026

Recent data from The Money Charity shows that the average total household debt levels in the UK reached £67,350 in January 2026 and the average debt level per individual is £34,774. These figures reflect a very real trend: debt levels are continuing to rise across the UK, and more people are feeling the pressure in…

-

What happens when debt isn’t paid off?

What happens when debt isn’t paid off? Debt doesn’t usually spiral overnight. It often starts with a missed payment, a letter left unopened, or a period where money is simply stretched too thin. Many people who fall behind on payments didn’t expect to be in debt in the first place. If you’re unsure how your situation started, our guide on the common…

-

10 common reasons people get into debt in the UK

10 common reasons why people get into debt in the UK People get into debt in the UK for many reasons – often due to changes in income, rising living costs, health issues, or unexpected life events. Understanding the most common reasons people get into debt can help you recognise your own situation and take…

-

What’s the difference between gross and disposable income?

What’s the difference between gross and disposable income? When you’re trying to get a handle on your finances, it’s easy to get confused by the terms flying around, especially when it comes to your income. But what do the terms ‘gross income’, ‘net income’ and ‘disposable income’ actually mean, and more importantly, which one tells…

MoneyPlus Advice

Helping people struggling with debt

close

MoneyPlus Advice Articles

You are here:

- Home

- MoneyPlus Advice Articles